The challenges of growing overseas competition, cost of living pressures and the threat of further regulatory oversight are being met by Australia’s leading lottery and Keno operator – so far.

More than 2,000 years ago, the Chinese Confucian philosopher Mencius said friends are the siblings God never gave us. Those sage words ring ever truer in retirement when the opportunities to find friendship are more limited.

APRA ups scrutiny of unlisted property in super

From January 1, the Australian Prudential Regulation Authority (APRA) will enforce bolstered draft guidelines and principles that govern the way super funds value investments, including unlisted assets such as private equity and property.

APRA’s intervention comes after the regulator’s 2021 superannuation thematic review found existing valuation frameworks were in most cases inadequate. Moreover, board engagement was limited and super funds routinely accepted external valuations without challenging their appropriateness.

Investors have become increasingly critical of the strong performance of unlisted assets given the bifurcation in valuation from similar listed investments.

This is against the backdrop of interest rate hikes by major central banks globally, which have recalibrated − mostly downwards − the valuations of listed property, equities and debt.

The latest data from the Property Council of Australia and the Property Funds Association revealed unlisted property had appreciated 18.7 per cent in the year to September 30. Conversely, listed Australian property declined 19.7 per cent over the same period.

Put another way, unlisted property outperformed listed peers by more than 38 per cent.

Even stacked up against other asset classes, the performance stands out. Over the past five years, unlisted property has returned 15.8 per cent annually, compared with just 6.9 per cent for Australian equities and -0.2 per cent for listed property.

Private markets lag

It should be noted that listed assets are valued by the market daily, whereas unlisted assets are valued periodically, usually either quarterly or annually. This means changes in valuations take time to flow through.

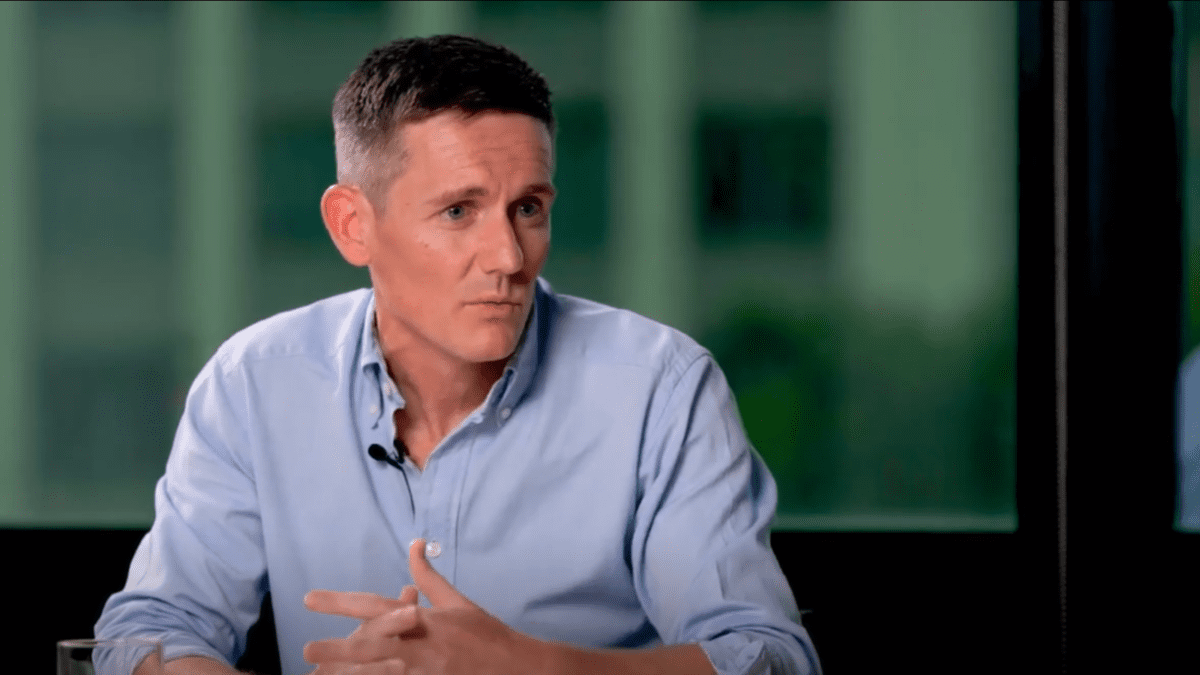

Pete Robinson (pictured), head of fixed income investment strategy at Challenger, said that despite the rapid increase in interest rates, valuation remains robust. He cited the recent 0.5 per cent appreciation in Charter Hall’s property assets despite their trading at a mid-teens discount to net asset value.

“A lack of transactional activity has likely delayed any reductions in valuation, though that is likely to change through 2023,” Robinson added.

Growing market scepticism also comes as a result of global alternative asset manager Blackstone restricting redemptions on its flagship Blackstone Real Estate Income Trust, the largest unlisted property fund in the United States.

In a December note, listed property manager Resolution Capital said the redemption restrictions suggested a broader pause or possibly even a reversal in flows to unlisted real estate markets.

“Most appraisal-based private real estate valuations are not representative of changes to market investment hurdle rates,” Resolution said. “More pointedly, private real estate values should fall.

“Whilst we aren’t privy to the finer details of unlisted property fund valuations, based on easily observable market data it is obvious that many high-quality listed REITs with strong balance sheets are trading at 15-30 per cent discounts to unlisted property funds investing in similar property types.”

APRA’s new standards are principle-based rather than prescriptive, giving super funds some wiggle room. Responsible entities will have until March 17 to provide consultation on the new guidelines.