The challenges of growing overseas competition, cost of living pressures and the threat of further regulatory oversight are being met by Australia’s leading lottery and Keno operator – so far.

More than 2,000 years ago, the Chinese Confucian philosopher Mencius said friends are the siblings God never gave us. Those sage words ring ever truer in retirement when the opportunities to find friendship are more limited.

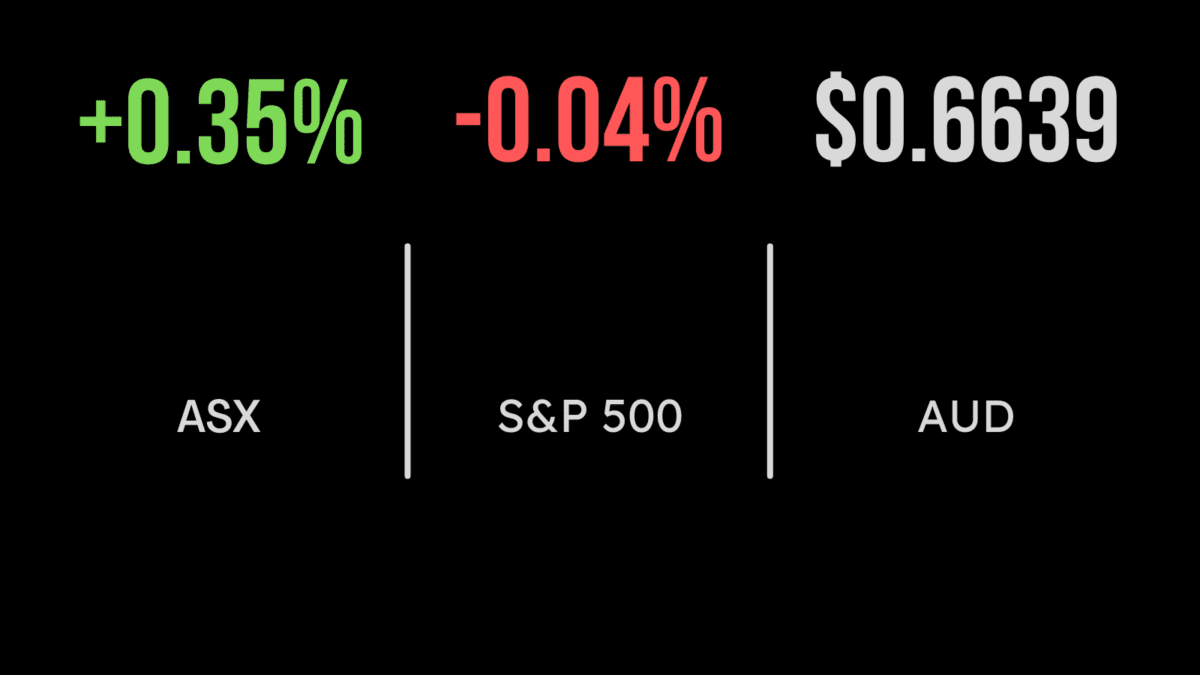

ASX edges to new record close, fourth weekly gain

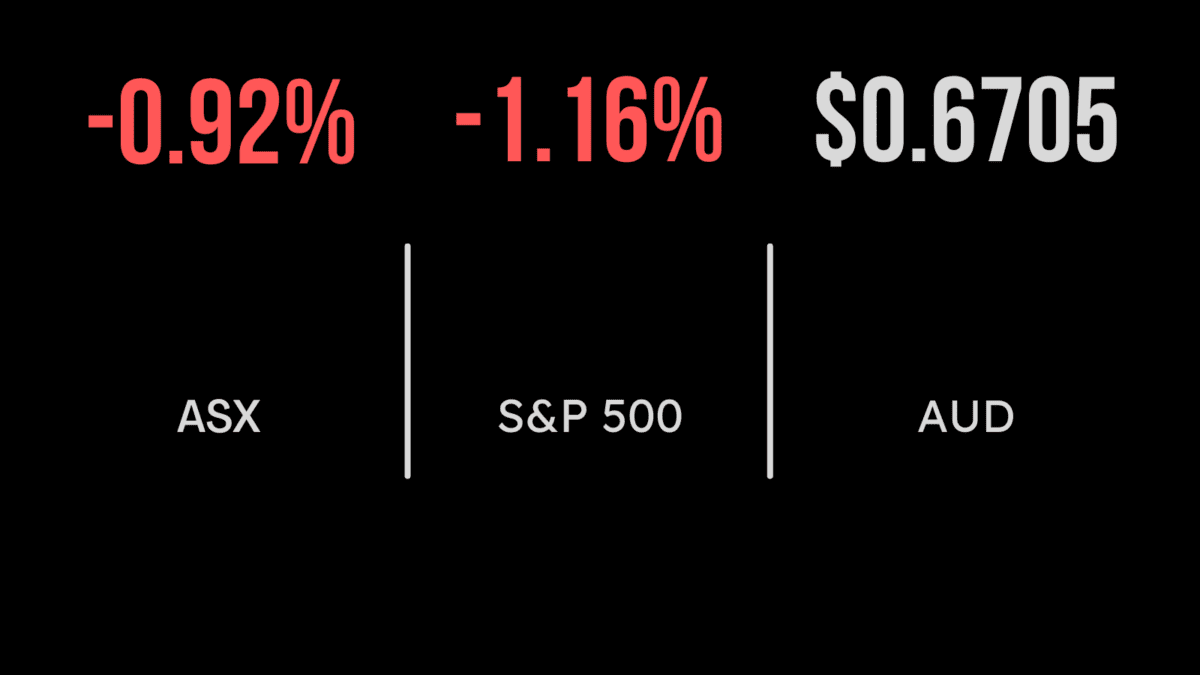

ASX finishes at fresh record, shrugs off inflation threat, tech, gold rally

The ASX 200 (ASX: XJO) finished +0.1% on Friday, taking the market 0.2% higher for the week and ultimately finishing at another all-time high.

On Friday, it was the gold miners responding to the expected inflation data in the US. Resolute Mining Limited (ASX: RSG) and Newcrest Mining Ltd (ASX: NCM) jumped 7.7% and 3.1% respectively, as the price of gold exceeded US$1,900 once again.

On a company-specific level, Premier Investments Limited (ASX: PMV), owner of Smiggle, was just 0.4% higher despite confirming sales would be 16% higher than 2019 levels and 70% higher than 2020.

Management noted the decision to stock up on inventory and invest in its supply chain as key drivers of the strong performance.

Over the week, it was the financial sector that struggled, with the likes of National Australia Bank (ASX: NAB) falling 3.8%.

The highlights by far were in the IT and real estate sectors, up 7% and 3.0% respectively, with Altium Limited (ASX: ALU) skyrocketing 28.6% after receiving a takeover offer.

Iress Ltd (ASX: IRE) shares climbed 20.4% higher on Barrenjoey rumours.

Bond rates fall most in a year, Nasdaq rallies on tech, value rally slows

The Dow Jones finished the week flat, with the index ending in the red for the first time in three weeks, down 0.8%.

Both the S&P 500 and the Nasdaq were higher, jumping 0.2% and 0.4% on Friday, taking their weekly gains to 0.4% and 1.9% respectively.

Eight of the eleven sectors within the S&P 500 finished higher, yet it was the big tech names that really drove the market.

Amazon.com Inc (NYSE: AMZN) added 4%, Twitter Inc (NYSE: TWTR) 2.5%, and Alphabet Inc (NYSE: GOOGL) 1.5% over the week, despite the inflation rate hitting 5%.

Despite expectations a spike in inflation would cause a market-wide sell-off, government bond yields actually fell, supporting markets but particularly technology valuations. The fall was the most in over a year.

Whilst the consensus has moved to the ‘value’ trade being the greatest opportunity, could the rally be over before it even started?

Elsewhere, cybersecurity remains a key focus for businesses across the globe with a number of recent high-profile hackings.

Overnight, McDonald’s Corp (NYSE: MCD) reported that hackers had stolen some customer data.

Inflation is here, or is it? Eye-watering valuations, public expectations grow

The talking point of the week and perhaps most of 2021 has been the threat of inflation.

Thursday night’s CPI print in the US confirmed it, with prices rising 5% on 2020 levels, yet all hell didn’t break loose.

In fact, sharemarkets rallied and bond yields fell, the opposite of many doomsayers’ projection in recent months.

Inflation has been defined in many ways by most specifically as a general rise in the price of goods and services in the economy.

Thursday’s result was anything but, in fact, the increasing price of used car sales contributed over a third to the result, with energy prices also a key input.

Yet with energy prices coming off a near-zero base in 2020 and used cars clearly not a must-have by most Americans, this is clearly not a ‘general’ rise in prices; hence the market reaction.

Less mainstream commentators are now suggesting deflation may be a risk given the continued indebtedness, ageing demographic, and higher savings rates around the world.

This week also saw the public expectations of business leaders expand once again, with AUSTRAC launching proceedings against no less than four blue-chip Australian companies for money laundering issues.

And finally, it was the surge in valuations of everything from cryptocurrencies to our major banks.

Interestingly, Commonwealth Bank (ASX: CBA) currently trades at its most expensive level on a price-to-book basis in history according to global manager T. Rowe Price.